Speaking to families all over the country about private family banking, I’m always shocked to learn how little they understand about the eroding effects of Federal Reserve banking, and it’s impact on their personal economy.

Everyone is always concerned about the interest rate they are paying, yet they continue to pay the banks interest and fees for access to capital. And, rarely do they question the fees and the costs associated with financing.

Many will research the topic of the Federal Reserve and discover that the system is corrupt, but they feel trapped and frustrated. Fortunately, once people understand how they can take control of the banking function in their lives, their mood changes and they start to get excited.

If there were only one thing to learn about banking it would be easy, but it can get complicated, and the wealthy bankers like it when we’re confused.

So, if you could simplify everything, which is better? Federal Reserve Banking or Private Family Banking? First you have to understand these major differences.

Federal Reserve Banking – Tyranny, Inflation and Bondage

Federal Reserve Banking

Federal Reserve System

Fractional Reserves

Financial Tyranny

Serfdom

Private Family Banking – Liberty and Freedom

Private Family Banking

Private Family System

Capital Reserves

Financial Freedom

Truth

Imagination

Imaginenever having to depend on banks for money. Meaning that you have freedom from bank qualifying and government red tape.

What if you had access to capital at any time for opportunities? Have you ever considered starting a business? Investing in real estate?

What if you could give more to your church or causes you care about?

What’s the difference in banking?

Control

Reserves

Liberty

The banking function is the key component when discussing control. Most people think because they maintain the account they have control. However because of increasing regulation like the Dodd-Frank Act, disquised as consumer protection, the financial institutions control the capital and the bankng function.

During a Brookings webinar, Former Federal Reserve Chair Janet Yellen, said “I personally think we need a new Dodd-Frank.” and “We need to change the structure of FSOC and beef up its powers…”

Controlling it is the most important thing you can do over your lifetime.

~Nelson Nash (Bestselling Author of Becoming Your Own Banker)

What are reserves?

Federal Reserve banks work on the fractional reserve system. Banks are required to only hold 10% of their deposits on reserve, meaning they can gamble with the other 90%. And, if they lose… Well that’s what bailouts are for right?

Ironically, banks store their 10% (Tier 1 Capital) in specific life insurance contracts called BOLI or Bank Owned Life Insurance.

On the other hand, Family Bankers can also own and utilize specific types of life insurance contracts as a place to store their capital reserves. This means they can control the contract and can set the terms for financing.

At the end of the day, if all of your money is in the the federal system, you will pay more, have less available, and keep less for your family.

We typically pay for the major purchases we make with credit through other banking institutions. While debt is the outcome for the individual, credit expansion is the much deeper problem with banking.

This creates a problem for everyone because of fractional reserve banking. Traditional banks lend more than what is on deposit with them, and in doing so expand the supply of money via credit.

The problem is so widespread that a solution seems impossible, but there is a solution. This solution’s only requirement is the action of a single person or family acting in a way to not only help themselves, but in doing so also helps society.

Fractional reserve banking leads to obligations that can not be fulfilled from the outset. The borrower and the depositor actually become owners of the same money.

Financing

When it comes to financing, consumers today face many problems when making major purchases. Questions arise that often lead to confusion.

Pay cash?

Lease?

Finance?

What about the terms and the interest rate?

THE VOLUME OF INTEREST IS THE REAL ISSUE, NOT THE ANNUAL PERCENTAGE RATE.

R. Nelson Nash, Becoming Your Own Banker

If you were offered a loan for an unlimited amount, but the terms were unknown, would you take that loan? That is the loan most Americans are subject to with their Qualified Retirement Plans (i.e. 401k, IRA, SEP, etc).

These plans are dictated by the Internal Revenue Service (IRS), and managed by the financial institutions (traditional banks). They make the rules and they control the assets.

The account balances in these government qualified plans have a tax liability. This tax debt must be paid within a structured time window or be subject to an additional tax penalty.

Meanwhile the average family finances their major purchases on credit, while their money is locked up inside these government plans. Thus creating additional problems of stress and lost opportunities.

Bank Incentives and Wealth Transfers

Financial institutions and banks are forever creating incentives to coax consumers into financing with them. They offer initial low rates, gifts and convenience. But sadly, many times consumers have no idea what they are really signing up for.

Financing will be one of the largest transfers of our wealth over our lifetime, so understanding how to pay for the items we purchase should be of prime importance.

THE PROBLEM IS ALL THESE ITEMS ARE FINANCED THROUGH OTHER BANKING ORGANIZATIONS.

R. Nelson Nash, Becoming Your Own Banker

Privatized Family Banking is the Solution

Privatized Family Banking is a valid solution and alternative to traditional financing. Also known as Infinite Banking or IBC, this private method for financing, provides the ability to create generational wealth without bank rules or qualifying.

What if you discovered that interest rates were not the problem, and that the volume of interest we pay was the real issue we should be concerned with?

In his bestselling book, Becoming Your Own Banker, Nelson Nash explains why the volume of interest we pay is much more important than the annual percentage rates.

Use available savings and cash-flow to fund your “family bank”

Use only dividend-paying, permanent life insurance

Capitalize and establish your plan over time

Use the method to finance your major purchases

Expand your system through a system of banks to increase wealth

Business can use the concept for cash-flow and equipment financing

To learn even more about banking and how you can utilize it in your life, follow this link and sign up for this free IBC video training.

Like our blog? Leave a comment to let us know. Have a question? Ask in the comment section, and we’ll do our best to answer it for you.

Until next time, Barry Page Family Banker and IBC Authorized Practitioner

Barry Page is a Registered Financial Consultant and the Managing General Agent and Founder of Legacy Insurance Agency, PLLC. His specialty is life insurance and educating others on how Infinite Banking works.

How To Become Your Own Banker Using the Power of Whole Life Insurance

In this post I’m going to share with you the secrets of private family banking and how to become your own banker using the power of whole life insurance. Keep reading to learn the secrets for creating generational wealth for your family.

What if you and your family never had to depend on a bank or finance company ever again? If that sounds interesting to you, then keep reading, because I’m going to explain in simple terms, Private Family Banking, and how you can become your own banker.

What is Family Banking?

When discussing Family Banking, we are referring to the method of using permanent, dividend paying, cash value life insurance policies to create a multi-generational banking system.

This Family Bank is private, and grows automatically while shielding your dollars from predators. It also provides opportunities for family members to participate in growing the family’s wealth by financing their major purchases, and possibly investments, without traditional credit reporting.

How To Practice Private Family Banking

You use available savings and cash-flow to build your own ‘bank’

You finance major purchases through your ‘bank’ with loans

You repay your ‘bank’ interest the same way as a traditional bank

You can build a system of ‘banks’ to increase your family’s wealth

Private family banking is not a physical bank. it is a thought process that involves the functions of a bank using custom designed life insurance.

Family Bankers Secrets

The elite and wealthy have understood the secrets of banking for years. Think of the Rockefellors, Vanderbilts, Kennedys, Morgans and Rothschilds.

In more modern times, there’s another famous family you may have heard of that used private life insurance to finance their empire, Walt Disney.

Walt Disney used funds from his life insurance policy, after the banks refused to lend him money to start a theme park, the now famous Disneyland.

Walt Disney

To understand family banking, it’s imperative to first understand how your money flows. Our money flows through our lives and throughout the world, just as water flows through our bodies and the oceans.

Your ability to control your cash-flow is the keyto understanding how to become your own banker.

The very first principle that must be understood is that you FINANCEeverything that you buy – you either pay interest to someone else or you give up interest you could have earned otherwise.” ~R. Nelson Nash

The Problem…

The problem is that all these items are financed by other banking institutions. This means that the interest portion of every dollar spent is perpetual. The volume of interest is the real issue, not the annual percent rates.

The average American family spends about 30% of their income on interest and fees. Compare that to the savings rate of most Americans of about 5% and you can see the discrepancy.

There’s a huge headwind overpowering our ability to create wealth. So, if we could change those ratios to where we were saving 20% or more of our income, while reducing our interest payments, then we could create a perpetual tailwind.

Some of you may be thinking that you pay cash for all of your major purchases and have no need for finance. That’s fine, but the problem is when you pay cash, you lose the ability for that money to ever work for you again. Once it’s out of your system, it can’t earn a return for you or your family, it’s gone forever.

The Solution

Private Family Banking can be the solution to your financial problems. You can have your money work harder by providing you with protection, savings and financing options.

You can create your own system for financing all of your purchases over your lifetime, where you recapture payments that you would normally make to others.

Learning how to redirect those payments into your own financial system is what makes the difference. This can be achieved over time with practice and help from a professional.

How Family Banking Works

Family banking works best through a custom designed, dividend paying, participating whole life insurance policy from a mutual life insurance company. You can not purchase these products direct from the company and they should be custom tailored by an experienced banking agent to fit your financial goals.

Because you have to qualify for life insurance health wise and financially, the companies underwrite each policy. If you are in poor health, you still have alternatives. Contact an agent to learn more.

By utilizing time tested and proven whole-life insurance , you can in essence create a private family bank, never having to depend on traditional banks or the government for money or loans again.

These custom designed Whole Life policies are designed to accentuate cash-value growth, especially in the early policy years. Depending on your state, these policies can also provide other benefits including creditor protection, disability, long term care and tax benefits.

These custom designed policies function like a bank…

By you making deposits and loans

By giving you access to capital

By allowing liquidity, use, and control of your money

By earning a predictable return over time

Saving versus Investing

For the most part, all of the large banks and financial institutions are trying to lure you in to their latest investments, so they buy advertising to convince you that you need to invest with them.

But, we’re not talking about investing here, because that involves risk. And, I’m assuming you don’t want to risk your hard earned money. What I’m going to share with you is the safest place to save money and have it work harder for you.

And… there’s hard evidence that goes back over a century. So, this is not a hypothetical projection of what could happen, it is a predictable illustration of what will happen.

Back to saving… When you think about how you should save, you have to consider many factors. These factors may span a lifetime or they may be for a short period of time. But, even if your reason for saving is short term, eventually you’ll have a need to save again. So, why not use a savings vehicle that allows for uninterrupted compounding?

Most people are familiar with compound interest, but the term uninterrupted compounding often causes some questions.

About Life Insurance

Life insurance companies are some of the safest institutions in the world. For centuries, life insurance policies have provided protection and savings to families and businesses.

Actuaries design and build policies with mortality tables that are based on actuarial data from 10 million selected lives. Lives are selected based on even more data from underwriting statistics, in other words lives that have been underwritten.

How Do Dividends Work?

Mutual life insurance companies use data to calculate annual dividends based on the company’s current mortality experience and their operating expenses.

Dividends are not guaranteed, however they have been paid consistently for well over 100 years by most mutual companies. Dividends have actually increased due to significant increases in longevity.

Why park money in life insurance?

Wherever you park your money, ultimately the reason for doing so is usually for someone to someday be able to spend it. The hard part is figuring out how you can get the most benefits while your money is parked.

It really doesn’t matter where you are in life, the one financial tool that covers all life spans is whole life insurance. That’s because it’s not correlated to the markets and it’s predictable. It protects from loss and solves financial problems.

If you’re just getting started in life, you may look at it as a forced savings plan. The beauty is that it gets better with age. So, as your needs change you’ll find that you can get multiple uses of your same dollars and create generational wealth.

Stewardship

Instead of just handing over your money to your children and grandchildren, a Family Bank can lend them money to teach them financial responsibility. This will in turn increase their success and aid in their independence.

Adult children can also take on the role of stewards and become producers of family wealth, rather than consumers, this distinction is crucial.

So, let’s review Private Family Banking…

Protects your family and business from wealth transfers

Allows tax free access to capital for any reason

Provides a pool of capital for financing

Hedges your dollars against inflation

Can reduce your tax liabilities

Creates a financial legacy

Teaches stewardship

Now that you know this, why would you want to turn your hard earned money over to someone else’s bank? And then have to qualify for a loan, and pay them interest to borrow money???

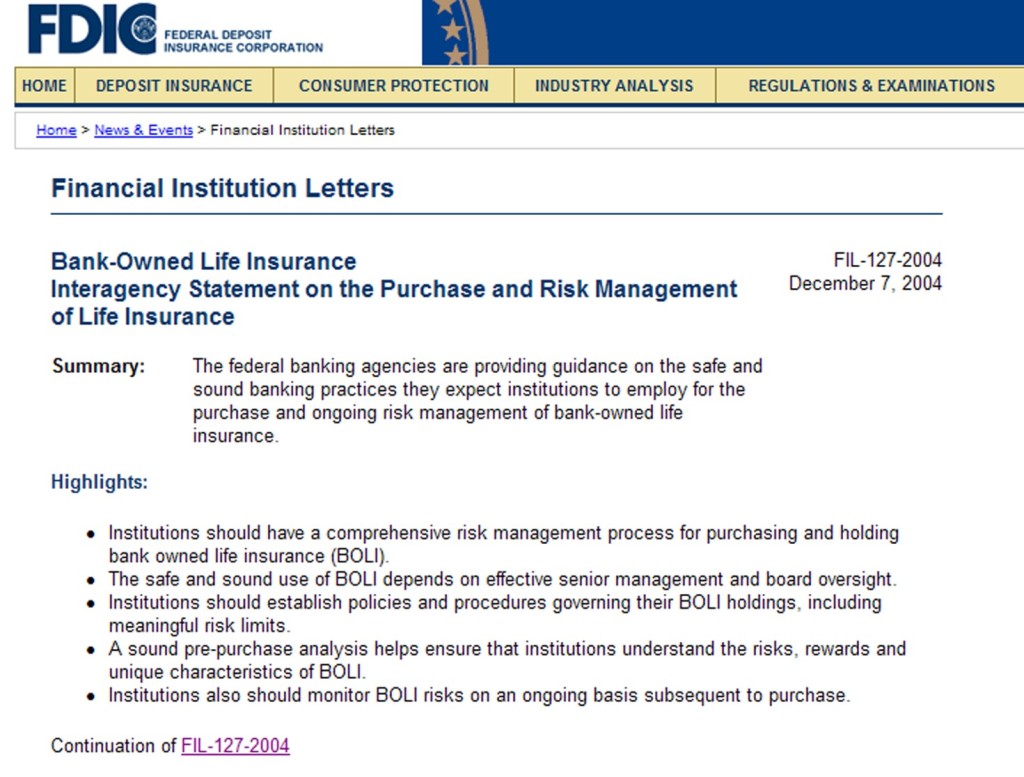

The Dirty Little Secret

Here’s the dirty little secret about banking and life insurance… The Big Banks own more life insurance than anyone, it’s called BOLI or Bank Owned Life Insurance. The FDIC even recommends they do.

FDIC Recommends BOLI

When you learn how to become your own banker, you can escape the enticement of the banking monopoly and build your own wealth privately.

“The way to get started is to quit talking and begin doing.”

~Walt Disney

Just follow the steps below and get started with “family banking”.

Get Started with Private Family Banking in 5 Easy Steps

Contact an approved family banking agent in your area

Until next time, start banking! Barry Page Infinite Banking Practitioner

Barry Page is a Registered Financial Consultant and the Managing General Agent and Founder of Legacy Insurance Agency, PLLC. His specialty is life insurance and educating others on how Infinite Banking works.