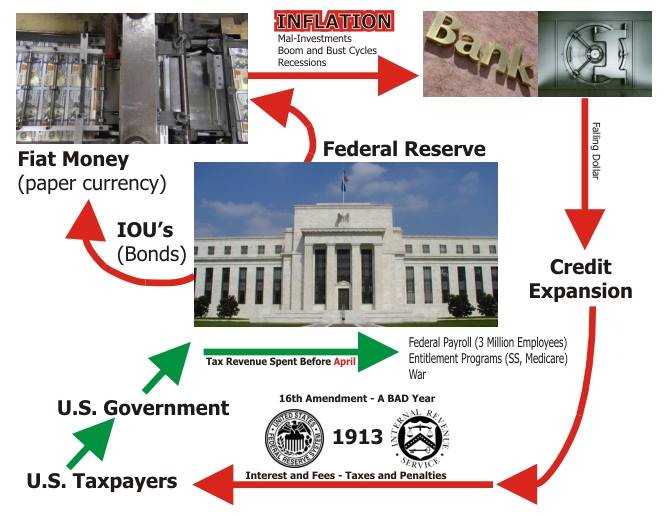

We typically pay for the major purchases we make with credit through other banking institutions. While debt is the outcome for the individual, credit expansion is the much deeper problem with banking.

This creates a problem for everyone because of fractional reserve banking. Traditional banks lend more than what is on deposit with them, and in doing so expand the supply of money via credit.

The problem is so widespread that a solution seems impossible, but there is a solution. This solution’s only requirement is the action of a single person or family acting in a way to not only help themselves, but in doing so also helps society.

Fractional reserve banking leads to obligations that can not be fulfilled from the outset. The borrower and the depositor actually become owners of the same money.

Financing

When it comes to financing, consumers today face many problems when making major purchases. Questions arise that often lead to confusion.

- Pay cash?

- Lease?

- Finance?

What about the terms and the interest rate?

THE VOLUME OF INTEREST IS THE REAL ISSUE, NOT THE ANNUAL PERCENTAGE RATE.

R. Nelson Nash, Becoming Your Own Banker

If you were offered a loan for an unlimited amount, but the terms were unknown, would you take that loan? That is the loan most Americans are subject to with their Qualified Retirement Plans (i.e. 401k, IRA, SEP, etc).

These plans are dictated by the Internal Revenue Service (IRS), and managed by the financial institutions (traditional banks). They make the rules and they control the assets.

The account balances in these government qualified plans have a tax liability. This tax debt must be paid within a structured time window or be subject to an additional tax penalty.

Meanwhile the average family finances their major purchases on credit, while their money is locked up inside these government plans. Thus creating additional problems of stress and lost opportunities.

Bank Incentives and Wealth Transfers

Financial institutions and banks are forever creating incentives to coax consumers into financing with them. They offer initial low rates, gifts and convenience. But sadly, many times consumers have no idea what they are really signing up for.

Financing will be one of the largest transfers of our wealth over our lifetime, so understanding how to pay for the items we purchase should be of prime importance.

THE PROBLEM IS ALL THESE ITEMS ARE FINANCED THROUGH OTHER BANKING ORGANIZATIONS.

R. Nelson Nash, Becoming Your Own Banker

Privatized Family Banking is the Solution

Privatized Family Banking is a valid solution and alternative to traditional financing. Also known as Infinite Banking or IBC, this private method for financing, provides the ability to create generational wealth without bank rules or qualifying.

What if you discovered that interest rates were not the problem, and that the volume of interest we pay was the real issue we should be concerned with?

In his bestselling book, Becoming Your Own Banker, Nelson Nash explains why the volume of interest we pay is much more important than the annual percentage rates.

How To Become a Family Banker:

- Educate yourself on Privatized Banking

- Schedule a meeting with an Authorized Infinite Banking Practitioner

- Use available savings and cash-flow to fund your “family bank”

- Use only dividend-paying, permanent life insurance

- Capitalize and establish your plan over time

- Use the method to finance your major purchases

- Expand your system through a system of banks to increase wealth

- Business can use the concept for cash-flow and equipment financing

To learn even more about banking and how you can utilize it in your life, follow this link and sign up for this free IBC video training.

Like our blog? Leave a comment to let us know. Have a question? Ask in the comment section, and we’ll do our best to answer it for you.

Until next time,

Barry Page

Family Banker and IBC Authorized Practitioner

Barry Page is a Registered Financial Consultant and the Managing General Agent and Founder of Legacy Insurance Agency, PLLC. His specialty is life insurance and educating others on how Infinite Banking works.